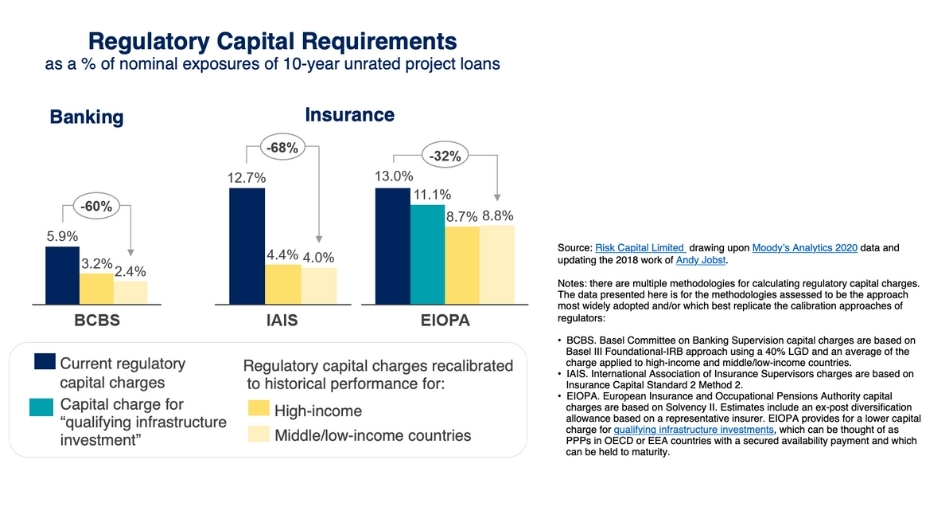

Regulatory capital frameworks require banks and insurers to put aside more capital for infrastructure investments than is warranted by these investments' historical credit performance, according to analysis recently commissioned by the Global Infrastructure Hub. Currently, regulatory authorities do not differentiate infrastructure investments from generic corporate exposures despite the data indicating the latter to carry greater risk.

By applying historical credit performance of infrastructure investments to calibration approach commonly used by regulators, we find that capital charges could be reduced by 60% to 70% for banks and insurers. This is true both for high-income country and middle- and low-income country infrastructure loans.

There are multiple methodologies for calculating regulatory capital charges. The adopted calibration approaches are designed to be as close possible in spirit and approach to those used by the following regulatory authorities: International Association of Insurance Supervisors (IAIS) and European Insurance and Occupational Pensions Authority (EIOPA) for insurers, and Basel Committee on Banking Supervision (BCBS) for banks.

For further details, see this study from Risk Control commissioned by the Global Infrastructure Hub.

{kind=link}